We use limited cookies

We use cookies where necessary to allow us to understand how people interact with our website and content, so that we can continue to improve our service.

View our privacy policyWe use cookies where necessary to allow us to understand how people interact with our website and content, so that we can continue to improve our service.

View our privacy policyBack in November of last year, following this blog and this story in the FT, the Public Accounts Committee asked a number of questions of the senior HMRC brass: Jon Thompson, HMRC’s CEO. And Jim Harra, HMRC’s Second Permanent Secretary (no, we don’t know either but it sounds and is important). (You can see the PAC’s questions and HMRC’s answers from question 88 here. And Jo Maugham QC addressed why he considered those answers to be unsatisfactory here.)

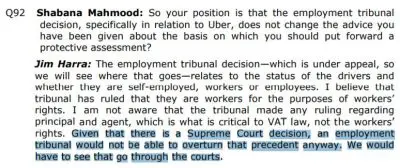

One of the answers Jim Harra gave was this:

We do not see how he can be read as saying anything other than that HMRC presently believes Uber not to be liable to VAT. And, indeed, this is consistent with what Uber says is the position.

And that is what we understood HMRC to have said in its decision refusing Jolyon Maugham’s claim for input tax.

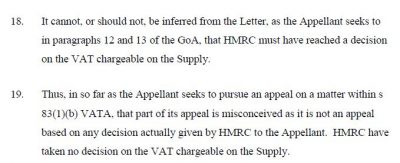

Earlier this week HMRC served its StatementofCase. But what it said was this:

Let me repeat the last sentence of paragraph 19: “HMRC have taken no decision on the VAT chargeable on the Supply.”

But that is simply and flatly inconsistent with the evidence Jim Harra gave to the Public Accounts Committee.

The Statement of Case pretends the situation is otherwise. It pretends that HMRC have not decided whether Uber is chargeable to input tax. And it embarks on that pretence because it wants to escape independent judicial scrutiny of its decision. There is, on the evidence, simply no other explanation.

There is no good explanation for why HMRC might adopt a position that leads to a loss of tax of, by our calculations, around £200 million per year. And in the absence of a good explanation you are compelled to a bad one. Last week direct evidence emerged that HM Treasury does put HMRC under pressure to go easy on other large US multinationals. We cannot identify any alternative candidate explanation that is consistent with the facts.

We will reply – likely next week – to HMRC and the specialist tax Tribunal making these points. And we will invite the Tribunal to refuse to allow itself to be used to advance what, on the evidence, looks to be a simple ruse.